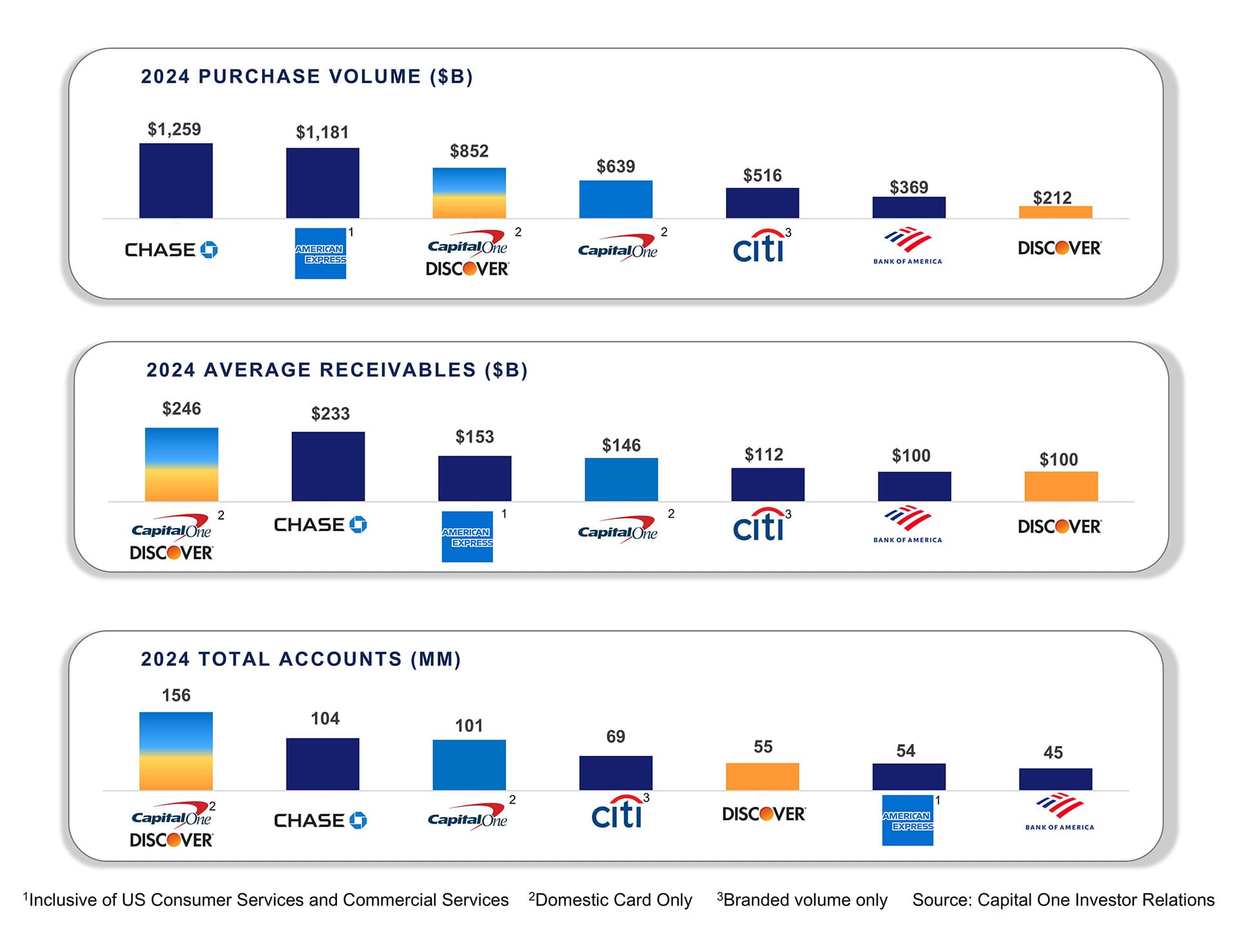

There is much to unpack with Capital One’s mega-acquisition of Discover. Equity analysts have covered it extensively from the announcement in February 2024 until this week’s closing. The synergy targets disclosed by Capital One are significant, ranging from the revenue unlock of Durbin-exempt debit interchange to reduced network expenses as the owner of the Discover network. In this note, we take a step back to assess what, if any, benefits might accrue to Capital One’s existing and prospective card partners over time. Note our emphasis on “over time” as we expect initial efforts to be focused mainly on Capital One’s proprietary card franchise, in addition to executing required changes to the Discover business in areas such as compliance and risk management. In other words, it may take time before we see the fingerprints of the Discover acquisition on Capital One’s partnership business unless a unique market opportunity presents itself.

To level set, Discover’s only card partnership is with the National Hockey League and associated teams. Unlike Capital One’s acquisition of HSBC USA in 2012, there is no stand-alone partnership business with the Discover acquisition. However, we draw one important similarity with the HSBC USA acquisition. Discover’s leading position in the cash-back segment is akin to HSBC’s strong position in the sub-prime segment at the time of acquisition. Put another way, Capital One will strengthen its cash-back presence with Discover, much like it fortified its non-prime leadership by acquiring HSBC.

In thinking of implications of the Discover acquisition in the card partnership space, we gravitate more to areas that are adjacent to card partnerships. Will the Discover franchise be a catalyst for Capital One Shopping and other ecosystem components (for example, Discover’s Pay with Rewards feature which was among the first to integrate with Apple Pay)? Will Discover’s direct relationship with merchants – large and small – prove to be an avenue in which Capital One can engage in card partnership discussions and more innovation as a closed-loop network – more curated offers, enriched cardholder experiences, expanded Pay with Rewards? Can the Discover network be the next breeding ground for Capital One to rethink card and non-card products, card acceptance, customer experience, and network operating rules (to name a few)? Of course, the notion of co-brand debit rewards is topical again, but we are more optimistic when coupled with a credit card partnership and suspect that Capital One will pick its spots.

There are countless considerations and nuances on the network side of card partnerships, not the least of which is that the selection of a payment network is made (or heavily influenced) by the non-bank partner. The remaining term of existing network contracts, exclusivity provisions, and financial incentives just add to the consideration set. Of course, there are broader and more significant strategic issues – will partners find the Discover network to be appealing in a partnership context and if so, how? Will certain co-brand partners value the three-party network as a form of protection or a hedge from potential interchange regulation? Would Capital One consider network-only arrangements in direct competition with Visa and Mastercard, an effort not pursued for some time by Discover? Speaking of Visa and Mastercard, both networks count Capital One as a large bank partner with important elements of Capital One’s strategy relying on international acceptance and the brand reach of its current networks. This dynamic is another reason we suspect Capital One will be disciplined in its network choices after its initial synergy-driven actions, but rest assured it did not acquire Discover to be passive with the network.

Granted, most of the implications on partnerships we cite are incremental and perhaps boring in the short-term which begs the question of what could be transformational. With both issuing and now network assets, Capital One could add new or enhanced components to its ecosystem given the installed base of merchants (e.g., relationships, connectivity, value chain) and deep visibility into the cardholder side. As a company founded and grounded in information management, the prospect of having a closed loop network must be alluring. Unconstrained by timing and resources, it is exciting to think of potential partners with significant scale and geographic reach who happen to be on their own journey of payments innovation. A closed-loop network owned by a bank that is also a full-spectrum lender with other complementary assets could have far-reaching implications – think of Apple, Google, Meta, Amazon, Shopify, and PayPal, let alone where we are in the evolution of digital wallets, embedded finance, BNPL, crypto, etc. Of course, those types of relationships are complex and take time to materialize, but Capital One is now in the game in a way that few are capable of playing. It may take time, but the potential is as exciting as Capital One decides to make it and the network is central to the end game. It’s not a matter of if, but when we will see aggressive, game-changing moves by Capital One whether in traditional card partnerships or some form of next-generation partnership powered by the Discover network.